The latest Glenigan Index of Construction Starts (covering projects under £100 million) for the three months to the end of January 2026 paints a cautiously mixed picture for the UK construction industry. Overall, the value of work starting on-site fell by 9% compared to the preceding three months, leaving construction project starts a significant 16% below 2025 levels.

Overall Construction Starts: Total industry activity declined by 9% over the last three months, leaving output 16% lower than January 2025 levels.

Residential Sector Downturn: Housing starts saw a sharp 24% drop quarter-on-quarter, finishing 32% down compared to the previous year.

Non-Residential Growth: Defying the broader trend, non-residential project starts rose by 6%, marking a 7% increase year-on-year.

Utilities & Civil Engineering: While civil engineering remained stable, the utilities sub-sector experienced a significant growth surge, driven by national infrastructure requirements.

What This Means for Construction Recruitment and Contracts

These shifts in the UK construction market are critical for project planning and construction recruitment strategies in early 2026. The data suggests a pivot in demand:

Skills Shift: Workforce demand is migrating from traditional housebuilding to specialised civil engineering and utility projects.

Contract Opportunities: Firms should target the non-residential pipeline, where project volume is currently outperforming residential schemes.

Market Resilience: Despite the residential slump, the surge in utilities highlights a robust area for long-term investment and job security.

UK Housebuilding Market Analysis: 2026 Residential Sector Downturn

The residential construction sector remains the primary drag on the UK industry’s overall performance. Latest figures show that overall residential starts plummeted by 24% in the most recent quarter, representing a staggering 32% decline compared to 2025 levels.

The private housing market has been most severely affected by the current economic climate:

Activity is down 38% compared to the same period last year.

New project starts fell by 30% against the preceding three months.

This downturn creates a high-risk operating environment for construction firms reliant on housebuilding contracts and site managers overseeing new-build residential schemes

Social Housing Recovery Stalls

Social housing projects have failed to provide the expected counterbalance:

Output is currently lagging 9% behind both the previous quarter and year-on-year 2025 figures.

Funding and regulatory transitions continue to delay the commencement of new affordable housing developments.

Why UK Housebuilding Starts are Stagnating

The root causes of this “housing doldrums” are structural and driven by market caution:

Investor Hesitation: Private developers and institutional investors are pausing major commitments until stronger homebuyer demand signals emerge.

Allan Wilen, Economic Director at Glenigan, highlights that there is “hope on the horizon” for the sector. The latest CIPS survey supports a cautiously optimistic outlook, noting that the contraction in UK construction activity is finally slowing as supply chains stabilise. This shift, marked by more predictable lead times and rising business confidence, suggests that the industry is preparing for a recovery despite the recent dip in project starts.

For firms navigating the 2026 construction market, these indicators suggest the pipeline is stabilising. This moderation is often the first sign of a transition toward a growth cycle, particularly in the non-residential and infrastructure sectors.

Non-Residential Construction: Office, Industrial, and Education Lead the Way

Non-residential construction continues to demonstrate resilience, providing positive news for contractors, commercial fit-out specialists, and those tracking commercial construction job opportunities.

Office Construction

Commercial office construction remains on an upward trajectory, rising 7% against the preceding three months and an impressive 21% year-on-year.

For commercial construction professionals and specialist subcontractors in the office fit-out and M&E sectors, this sustained growth in office project starts represents a tangible source of ongoing work.

Industrial and Distribution Construction

Industrial construction remained robust, posting a 2% increase against the preceding three months and standing 10% ahead of last year.

Education sector construction was a standout performer, rising 5% during the Index period and a remarkable 34% year-on-year.

For construction consultancies and contractors specialising in public sector projects, education represents one of the most active and growing areas of the current UK construction project pipeline.

Retail, Hotel, Leisure, and Community

Retail starts rose by 14% against the preceding three months but remained 13% below 2025 levels. Hotel and leisure starts climbed by nearly a quarter (24%) quarter-on-quarter, yet still sat 12% below the previous year. Community and amenity starts dipped slightly (3%) during the Index period but remained 4% ahead of 2025 figures.

UK Regional Construction Performance

Regional performance varied considerably across the UK during the period:

London was the clear standout, with construction starts rising 41% against the preceding three months and finishing 33% up year-on-year

East Midlands and North West delivered mixed results, rising quarter-on-quarter but still lagging behind year-ago figures.

West Midlands had a particularly difficult period, with starts falling 20% during the Index period and 23% year-on-year —

South East also struggled, declining 22% against the preceding quarter and sitting 15% below the previous year.

What This Means for Construction Jobs and Hiring in 2026

The Glenigan Index data has direct implications for those working in, or recruiting for, the UK construction industry:

Where construction job opportunities are strongest right now: Utilities and energy infrastructure, commercial office developments, education and public sector schemes, and industrial logistics projects offer the most active pipelines for construction work in early 2026.

Where caution is warranted: Private housebuilding and social housing remain deeply subdued. Infrastructure project starts have also fallen sharply. Contractors and trades professionals heavily reliant on these sectors will need to diversify their project exposure or consider pivoting towards growth areas.

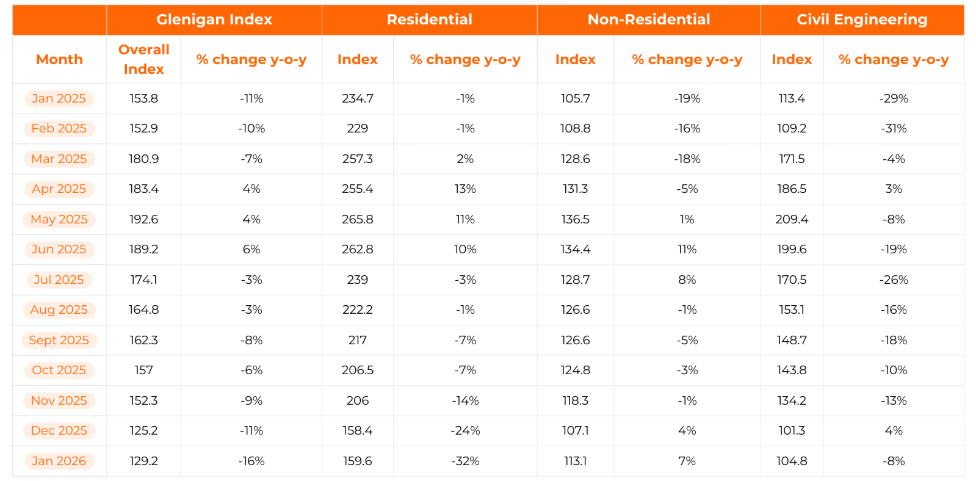

Glenigan Index Monthly Data Table: January 2025 – January 2026

About the Glenigan Index

The Glenigan Index is one of the UK construction industry’s most authoritative and widely cited barometers of construction project activity. Covering all project starts under £100 million, it provides monthly insight into the health of the UK construction sector across residential, non-residential, and civil engineering verticals.

Frequently Asked Questions (FAQs) Construction Market 2026

What is the current state of the UK construction industry in 2026?

As of January 2026, the UK construction industry is experiencing a transitional phase. Overall construction starts for projects under £100 million fell by 9% compared to the previous quarter and remain 16% lower than January 2025 levels. While the residential sector struggles, non-residential sectors like offices and education are showing strong growth.

Why are UK housebuilding starts declining so sharply?

Residential construction starts plummeted 24% this quarter, driven by a 38% year-on-year drop in private housing. According to the Glenigan report, this stagnation is caused by investor hesitation, high mortgage rates affecting buyer affordability, and a delay in the impact of government planning reforms.

Which construction sectors are growing in 2026?

Despite the overall dip, several sectors are outperforming the market: · Education: Up 34% year-on-year, making it a top sector for public works. · Commercial Offices: Rose 21% compared to last year, driving demand for fit-out and M&E specialists. · Industrial & Logistics: Increased by 10% year-on-year due to ongoing e-commerce infrastructure needs. · Utilities: Showing a significant surge driven by national infrastructure requirements.

Where are the best construction job opportunities in the UK right now?

The strongest demand for construction recruitment is currently in London, where project starts surged 41% quarter-on-quarter. Professionals should focus on the utilities, commercial office, and education sectors, as these pipelines are currently more robust than traditional housebuilding.

Is the UK construction industry expected to recover in 2026?

Yes. While starts are currently down, Glenigan’s Economic Director Allan Wilen notes hope on the horizon. Stabilising supply chains and rising business confidence, as reflected in recent S&P Global / CIPS UK Construction PMI data, suggest the industry is bottoming out before a predicted growth cycle later in the year.

What does the Glenigan Index measure?

The Glenigan Index tracks the value of construction project starts in the UK for schemes valued under £100 million. It covers three broad sectors and is published monthly, offering a rolling three-month view of UK construction market activity.

Why have UK construction starts fallen in January 2026?

The primary driver is the sharp decline in residential construction starts, which fell 32% year-on-year and 24% against the preceding quarter. Private housebuilding has been particularly weak, with developers awaiting clearer signals of buyer demand and stronger mortgage affordability before committing to new schemes. Overall construction starts are down 16% on 2025 levels.

Which construction sectors are growing in the UK in 2026?

The strongest performing sectors in early 2026 include commercial office construction (up 21% year-on-year), utilities and energy infrastructure (up 68% year-on-year), industrial and logistics construction (up 10% year-on-year), and education sector construction (up 34% year-on-year).

Where are the best regions for construction jobs in the UK right now?

London is currently the strongest performing region for construction project starts, rising 41% quarter-on-quarter and 33% year-on-year. Construction in the East Midlannds is also performing well.

Will housebuilding recover in 2026?

Most industry analysts, including Glenigan's Economics Director, believe a meaningful recovery in private housebuilding is dependent on improved mortgage affordability, stronger buyer demand, and the conversion of government planning policy reforms into actual planning permissions and development starts. The outlook for late 2026 is more cautiously optimistic, but near-term conditions remain challenging.

What types of construction jobs are most in demand in 2026?

Based on the sectors showing the strongest project start activity, utilities and civil engineering operatives, groundworkers, pipeline and energy infrastructure contractors, commercial office fit-out specialists, M&E engineers, and education sector construction trades are amongst the most in-demand construction job roles in the UK in early 2026. Explore these latest construction job opportunities with Atkins Search, a UK-leading construction recruitment agency.

Data source: Glenigan Index of Construction Starts to the end of January 2026. All figures relate to projects under £100 million in value.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies. However you may visit Cookie Settings to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

PHPSESSID

session

This cookie is native to PHP applications. The cookie is used to store and identify a users' unique session ID for the purpose of managing user session on the website. The cookie is a session cookies and is deleted when all the browser windows are closed.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

_ga

1 year 1 month 4 days

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_ga_*

1 year 1 month 4 days

Google Analytics sets this cookie to store and count page views.

_gat_gtag_UA_*

1 minute

Google Analytics sets this cookie to store a unique user ID.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.